.png)

Rich and Naive? Building Singapore’s Cryptocurrency Scene Block by Block

- Rex Heng, Bryan Pak, and Finna Ng

- Aug 27, 2025

- 8 min read

In this Explainer, find out...

How does cryptocurrency technology work?

How is cryptocurrency regulated in Singapore?

What are the benefits and risks Singapore would experience from using cryptocurrency?

Introduction

In 2022, Sam Bankman-Fried’s cryptocurrency empire collapsed and S$377 million disappeared from Singapore’s state-owned multinational investment firm Temasek Holdings overnight, shocking investors and people across the region. Singaporeans have lost millions of dollars to crypto scams, and yet these digital assets have reshaped the global financial landscape, providing both new opportunities alongside significant volatility.

Emerging as a pioneering force in cryptocurrency regulation and innovation, Singapore has created one of the world’s most comprehensive regulatory frameworks for cryptocurrencies. This allows Singapore to balance itself as a regional crypto hub while protecting consumers from these new digital assets. In this article, we will explain Singapore’s approach to managing this new digital asset class, and examine what are some of the risks and benefits of this rapidly evolving financial asset.

How Does Cryptocurrency Technology Work?

Before learning what goes on behind the scenes in a cryptocurrency transaction, it is important to understand some of the technical jargons used.

Cryptocurrency is a digital payment system that operates independently of any central regulating authority when verifying transactions. Unlike physical money which is issued and managed by banks, cryptocurrency is secured by cryptography and uses public blockchains to record transactions.

Cryptography is the use of algorithms to obscure information, such that only those who are authorised to access this information have the ability to decrypt it. It is an important aspect of cryptocurrency because it protects sensitive information from hackers and malicious threat actors who aim to extort or embezzle cryptocurrency from other parties.

Blockchains are distributed ledgers shared across a network of computers that record information in blocks. Each block contains transaction data and a cryptographic link to the previous block, forming a chronological chain. As blockchains are decentralised, all nodes have equal access to transaction records.

Steps Involved In A Transaction

When a user wants to transfer cryptocurrency, he or she will open a cryptocurrency wallet. The user will enter a few details, namely the recipient’s public address, the amount to transfer, and an optional transaction fee in their wallet interface.

After the user submits the transaction, the transaction data is then hashed using a cryptographic algorithm, which creates a unique transaction hash. The sender’s private key signs this hash and generates a digital signature. This signature verifies the transaction was authorised by the sender without exposing the private key itself.

The signed transaction is then broadcast to the cryptocurrency network through many nodes. The nodes are responsible for checking the transaction. For example, if the format of the transaction is correct, if the digital signatures are valid and if the sender’s wallet has a balance that is greater than or equal to the amount transferred and the transaction fees. If the transaction is valid, it enters a waiting area for unconfirmed transactions known as a mempool, short for memory pool.

Next, consensus mechanisms are performed. There are two consensus mechanisms which are widely used in cryptocurrency: proof-of-work and proof-of-stake.

In proof-of-work, miners will group unconfirmed transactions into a block. They will then compete to adjust a nonce until a value is found that gives the block’s hash a certain difficulty level. The first miner to find a valid hash earns the transaction fee as a reward. The miner or validator who completes the block then broadcasts it across the network to other nodes. Other nodes will then validate the block by checking for a few factors. For example, if the hash meets the difficulty and if all transactions within the block are valid. If the block is valid, then nodes will append the block to the blockchain.

In proof-of-stake, validators will lock up a certain amount of cryptocurrency as collateral. The larger the stake, the higher the chance of being selected to approve transactions and create blocks. A validator is selected at random to propose a new block, and this block is validated and attested to by other validators. When a predetermined number or proportion of validators have verified that the block is accurate, it is finalised and closed. The validators are then rewarded with the transaction fee for their work.

How Is Cryptocurrency Regulated In Singapore?

In order to regulate the rapidly evolving cryptocurrency landscape, the Singapore Government has introduced two key legislative frameworks: the Payment Services Act 2019 and the Financial Services and Markets Act 2022.

Payment Services Act 2019

In 2019, the Monetary Authority of Singapore (MAS) introduced the Payment Services Act to regulate and license digital payment token (DPT) services requiring providers to obtain stricter licensing. This Act has granted the MAS formal powers to ensure fairer third-party access to payment systems, participation in common platforms and to enforce the adoption of common standards. This act regulates seven types of payment services, including digital wallets, money transfers, cryptocurrency exchanges, and merchant payment systems. Companies providing these services must obtain one of three license types depending on their transaction volume: a Standard Payment Institution license for smaller operators handling under S$3 million monthly, a Major Payment Institution license for larger providers exceeding these limits, or specialized money-changing licenses.

The Act grants MAS tools to ensure fair market access and prevent the payment system from becoming fragmented. Additionally, providers have to comply with Anti-Money Laundering and Know Your Customer requirements, including processes such as identity verification, transaction monitoring, and insurance requirements. Technology risks are further mitigated by rigorous cybersecurity measures and systems, including user authentication and data protection.

Financial Services and Markets Act (FSMA) 2022

In conjunction with the Payment Services Act, the Financial Services and Markets Act has been further revised, and expanded to to include all businesses that operate in Singapore, even if they only serve foreign markets. This creates additional safeguards against money laundering and countering the funding of terrorism.

The Act addresses a regulatory gap that had developed in Singapore's digital asset sector, as cryptocurrency companies were serving exclusively foreign customers, benefitting from Singapore's business environment and strong regulatory reputation without meeting local licensing requirements. Companies are thus strategically avoiding regulatory oversight, which could further expose Singapore to reputational damage if these businesses faced operational or compliance failures.

Digital Token Service Providers have to pay a fixed annual license fee of S$10,000, maintain a minimum capital of S$250,000 and must appoint a Singapore-based compliance officer, adhering to audit and reporting requirements. Major incidents must be reported to the MAS within one hour of occurrence, further tightening the regulation on foreign companies.

What Are The Benefits And Risks Singapore Would Experience From Using Cryptocurrency?

Risks

Though the Payment Services Act and FSMA provide regulatory frameworks to govern cryptocurrency operations, significant risks still arise that regulations alone cannot fully regulate. Cryptocurrency transactions are largely untraceable, and the currencies still remain extremely volatile.

Firstly, cryptocurrency scams have begun to represent a growing threat to less digitally literate or savvy individuals, where residents have lost up to a quarter of one billion to crypto-related fraud. This surge has contributed to Singapore’s broader challenge with financial scams, earning Singaporeans the unfortunate label of being “rich and naive”. Cryptocurrency transactions exacerbate this issue, as traditional financial protections and recovery mechanisms that safeguard consumers in banking simply cannot function with this digital asset.

Second, the very volatility that has enabled individuals to earn millions pose equally serious risks to cryptocurrency investors. Even major and well-established cryptocurrency exchanges experience severe volatility that often exceeds traditional equity markets by a factor of two to three. When the prices of stocks go down, cryptocurrency prices have been known to swing by up to three times that magnitude, creating unpredictable and potentially catastrophic losses. This volatility is compounded by the effects of market contagion. When investors see the prices of cryptocurrency go down, they rapidly attempt to sell all their holdings, triggering massive price drops across the entire financial system.

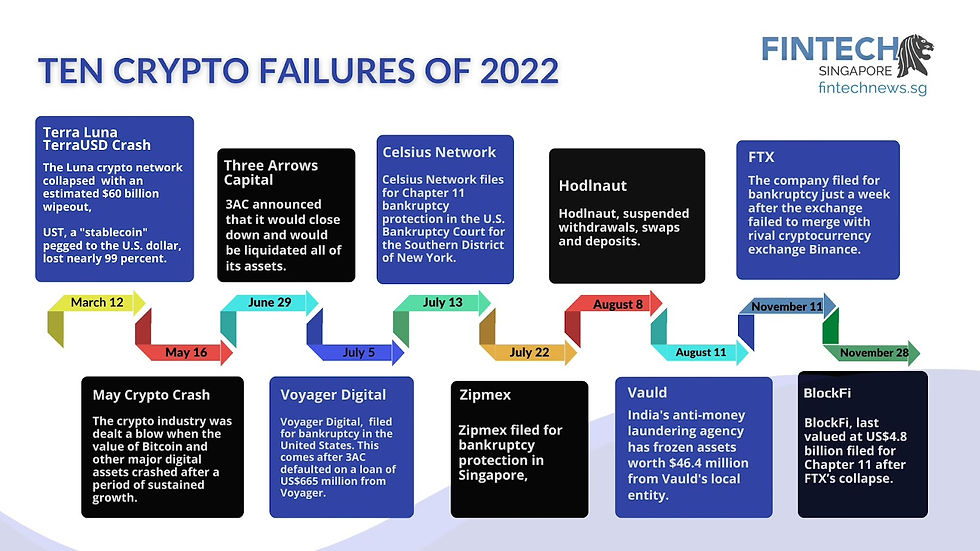

The dangers of platform failures are most apparent during the "Crypto Winter of 2022”, where four major DTPs collapsed in rapid succession — 3AC, Voyager, Celsius, and most infamously, FTX. This led to billions of dollars in investor losses worldwide. Temasek Holdings, Singapore’s sovereign wealth fund, lost its entire S$377 million investment in FTX, resulting in significant reputational damage as they failed to detect Sam Bankman-Fried’s alleged fraud. Platform failures highlight how seemingly reputable platforms can still face existential risks, and the rapid loss of investor capital in this nascent industry.

Policy Benefits

Financial Market Development

Singapore's regulatory approach to cryptocurrency has delivered measurable economic benefits, establishing the country as a leading digital asset hub. Clear regulatory frameworks encouraged institutional participation and attracted significant investment flows that strengthened Singapore's financial ecosystem.

A key milestone was when DBS Bank became the first Asian bank to offer cryptocurrency trading services to institutional clients in 2024. This made digital assets more accessible to traditional finance, and an established bank entering the cryptocurrency space lends credibility to the entire industry.

Singapore's licensing framework proved highly effective at attracting global operators. In 2024, the government issued 13 Major Payment Institution licenses, more than double the previous year's total. This demonstrates that cryptocurrency firms actively seek to operate in Singapore due to its clear and supportive regulations.

Status as a Regional Hub

The country has emerged as a premier destination for cryptocurrency events and innovation. TOKEN2049, the world's largest cryptocurrency conference, attracted 20,000 attendees to Singapore in 2024 alongside 800 related events. Such gatherings create substantial business opportunities and reinforce Singapore's position as the regional center for digital finance.

As more companies establish operations here, they bring valuable jobs, talent, and expertise that benefit the broader economy. This concentration of activity has transformed Singapore into a vibrant hub for cryptocurrency development and collaboration.

Investment and Innovation

Investment data reflects Singapore's growing prominence in the digital asset space. Singapore attracted approximately US$627 million in cryptocurrency funding across 88 deals in 2023, supporting over 1,200 blockchain startups. Programs like the Economic Development Board's Global Founders Programme have successfully drawn international entrepreneurs to Singapore, fostering a dynamic innovation ecosystem.

However, these positive developments must be weighed against the substantial risks outlined earlier. Singapore's long-term success will depend on whether it can sustain this growth while adequately protecting investors and consumers from cryptocurrency's inherent volatility and operational dangers.

Conclusion

Singapore's cryptocurrency regulatory framework through the Payment Services Act 2019 and Financial Services and Markets Act demonstrates a comprehensive approach to balancing innovation with consumer protection. These policies establish strict licensing requirements, anti-money laundering protocols, and enhanced oversight of digital payment token services.

However, for these regulations to truly be effective, market discipline and technological improvements are also necessary. Without continued vigilance from investors and better platform security measures, significant risks remain. The persistence of scams, extreme volatility, and platform failures like FTX—which cost Temasek Holdings S$377 million—show that regulatory frameworks alone cannot fully address cryptocurrency's inherent dangers.

Nevertheless, Singapore's regulatory approach marks an important step in creating a safer cryptocurrency environment. With continued cooperation between regulators, industry players, and investors, Singapore can maintain its position as a responsible leader in digital asset innovation.

This Policy Explainer was written by members of MAJU. MAJU is a ground-up, fully youth-led organisation dedicated to empowering Singaporean youths in policy discourse and co-creation.

By promoting constructive dialogue and serving as a bridge between youths and the Government, we hope to drive the keMAJUan (progress!) of Singapore.

The citations to our Policy Explainers can be found in the PDF appended to this webpage.

Comments